Book review slash top 5 takeaways of common stocks and uncommon profits by Philip Fisher.

《普通股與非凡利潤》一書評論及五大心得,作者菲利普·費雪。

00:07

This is the Swedish Investor.

這是瑞典投資者。

00:09

Takeaway number 1: Fisher's 15 points checklist.

心得一:費雪的15點檢查清單。

00:14

The core of any investment process is the task of deciding which companies to invest in.

任何投資流程的核心,都是決定投資哪些公司。

00:19

Fisher has created a checklist of 15 boxes, and to be considered a great investment, a company must tick most of them.

費雪創建了一份15點的檢查清單,一家公司必須勾選大部分項目,才能被視為優質投資。

00:26

1. The company should have services and slash or products which are addressing an expanding market.

1. 公司應提供服務或產品,以滿足不斷擴張的市場需求。

00:33

Today, an expanding market would be something like clean energy, autonomous drive, or perhaps machine learning.

如今,擴張中的市場可能包括清潔能源、自動駕駛或機器學習等領域。

00:41

2. Management must have a determination to develop new products.

2. 管理層必須有決心開發新產品。

00:46

No product can stay successful and yet remain the same forever.

沒有任何產品能永遠保持不變,卻又持續成功。

00:50

Perhaps Coca-Cola would disagree, but in almost every other industry, it holds true.

也許可口可樂會反對,但在幾乎所有其他行業,這一點都成立。

00:56

3. Research and development needs to be efficient.

3. 研發部門需要高效運作。

01:00

Look at how much the company have gained in revenue per spent amount in research.

觀察公司每花費一筆研發經費,能帶來多少營收增長。

01:05

4. Look for firms with an above average sales organization.

4. 尋找擁有優秀銷售團隊的公司。

01:10

This is the most basic activity of any company. Make sure it's handled well.

銷售是任何公司最基本的活動,務必確保其運作良好。

01:15

5. Pick companies with a handsome profit margin.

5. 選擇擁有可觀利潤率的公司。

01:20

Look at how much each dollar in sales produces incense in operating profits.

觀察每一美元銷售額能產生多少營運利潤。

01:25

The higher, the greater the cushion in bad times.

利潤率越高,在不景氣時的緩衝空間越大。

01:28

6. Not only do you want awesome profit margins today, but you also want to pick a company that does everything to maintain them in the future as well.

6. 不僅要追求當前的優秀利潤率,還要選擇能持續維持高利潤率的公司。

01:38

An important part of this is how efficient the company is in cutting its costs.

其中一個重要因素是公司在削減成本方面的效率。

01:42

7. Look for businesses that treat their employers like humans, not like cogs in a wheel or FTEs in an annual report.

7. 尋找將員工視為人才而非機器零件或年報中FTE(全職員工)的企業。

01:51

Most investors underestimate the importance of great labor relations.

大多數投資者低估了良好勞資關係的重要性。

01:56

8. If the relationship with blue collars are important, the firm's relationship with its executive personnel is vital.

8. 如果與藍領員工的關係很重要,公司與高管人員的關係則至關重要。

02:05

These are the people that can make or break any venture.

這些人能夠決定任何企業的成敗。

02:09

9. You want to invest in a business which has depth to its management.

9. 你應該投資於管理層具有深度的企業。

02:15

One man shows can be successful for a while, but organizations where people grow can stay successful forever.

個人英雄主義可能暫時成功,但能夠培養人才的組織卻能永續成功。

02:22

10. Look for companies with great cost analysis.

10. 尋找擁有出色成本分析的公司。

02:26

Without this, a firm cannot know where to allocate its resources most effectively.

沒有這一點,公司無法知道如何最有效地分配資源。

02:31

It's difficult to decide if a company is truly outstanding in this perspective, but it's easy to identify if they are deficient. Avoid the latter.

雖然難以判斷一家公司在這方面是否真正出色,但很容易發現他們是否有所不足。避開後者。

02:40

11. The company should be outstanding compared to its competition on industry-specific aspects.

11. 公司應在行業特定的方面相較於競爭對手表現出色。

02:47

What the business should be awesome at differs from one industry to the other.

企業應在哪方面表現出色,因行業而異。

02:51

For a retailer, for instance, it might be how they handle their inventory.

例如,對零售商來說,可能是他們如何管理庫存。

02:56

For an airline, it might be how efficient they are at pricing every available flying seat.

對航空公司來說,可能是他們如何有效地為每個可用的飛機座位定價。

03:05

12. Invest in a company with a long-range outlook on profits.

12. 投資於具有長期利潤展望的公司。

03:11

A few businesses create great profits today at the expense of profits tomorrow.

有些企業以犧牲明天的利潤來換取今天的高利潤。

03:17

For the long-term investor, this is undesirable.

對於長期投資者來說,這是不利的。

03:20

A company aiming for profits in the long run creates strong relations with their employees, their customers, and their suppliers.

以長期利潤為目標的公司會與員工、客戶和供應商建立良好的關係。

03:27

13. Seek out companies where your shares run a low risk of being diluted in the future.

13. 尋找未來股權稀釋風險低的公司。

03:34

Such companies have strong cash positions and or great borrowing opportunities.

這類公司擁有強大的現金儲備和/或良好的借貸機會。

03:39

14. You want to avoid firms where the management brag about good news as soon as they get a chance to, but don't reveal bad ones until absolutely necessary.

14. 你應該避開那些管理層一有機會就炫耀好消息,但對壞消息卻遲遲不願透露的公司。

03:50

15. Invest only in companies where the management have unquestionable integrity.

15. 只投資於管理層具有無可置疑的誠信的公司。

03:56

The management is much closer to the assets of the company than the investors, and the number of ways that they can benefit at the expense of the shareholders— that's you and me—legally, are infinite.

Therefore, this is the only one of the 15 points which is absolute.

因此,這是15點中唯一絕對的條件。

04:12

If it's not fulfilled, you should not invest.

如果不符合這一點,你就不應該投資。

04:16

Takeaway number two, the scuttlebutt method.

第二個重點,流言調查法。

04:19

After hearing about these 15 points, you probably ask yourself this.

在聽過這15點之後,你可能會問自己這個問題。

04:23

Where can I read about all this?

我可以在哪裡讀到這些資訊?

04:25

Unfortunately, the answer is, you can't.

不幸的是,答案是:你讀不到。

04:29

However, you can find the information you seek by applying the scuttlebutt method.

但是,你可以透過流言調查法來找到你想要的資訊。

04:55

The investment value at time zero equals to the sum from time one.

在時間零點的投資價值等於從時間一開始的總和。

05:03

How do you spend time at Tesla?

你在特斯拉如何度過時間?

05:05

What do you do? How do you get people excited about Tesla?

你做什麼?你如何讓人們對特斯拉感到興奮?

05:08

Is there room for possibly an even less expensive quality electric car experience?

是否有可能推出更便宜的優質電動車體驗?

05:14

Scuttlebutt is the technique of using and talking to main street resources to find out if a stock is worthy of your money or not.

流言調查法是一種利用和與主流資源交談的技巧,以確定一支股票是否值得你投資。

05:21

Such sources could be: 1. Suppliers of the company, 2. Customers of the company, 3. Research scientists within the specific industry that the company operates in, 4. Trade associations, and 5. Former employees.

Caution. Information from these people can be of immense value, but it's usually influenced by a bit of negativity.

注意。這些人的資訊可能具有極大的價值,但通常會受到一些負面情緒的影響。

05:47

After all, there's an underlying reason as to why their title is former employee instead of employee.

畢竟,他們的頭銜是前員工而不是員工,背後總有原因。

05:54

Here's another advice on how to apply scuttlebutt.

這裡有另一個關於如何應用流言調查法的建議。

05:57

Go to five companies within the industry that you are researching.

去你正在研究的行業中的五家公司。

06:01

Ask each of them about strengths and weaknesses of the other four firms.

向每家公司詢問其他四家公司的優缺點。

06:06

What will emerge from this information is a quite detailed picture about the industry and which company that will make a great investment.

從這些資訊中,你將能夠獲得一個相當詳細的行業圖景,並確定哪家公司是一個很好的投資選擇。

06:13

If competitors talk about your investment budget with respect and maybe even a bit of fear, you are one step closer of finding a great investment.

如果競爭對手在談論你的投資預算時帶著敬意,甚至有些許恐懼,那麼你離找到一個好的投資又近了一步。

06:23

Here are a few suggestions on how you can contact these people.

以下是幾個建議,告訴你如何聯繫這些人。

06:27

1. You could use LinkedIn.

1. 你可以使用領英(LinkedIn)。

06:29

2. You can use the contact information provided on the company's website.

2. 你可以使用公司網站上提供的聯繫資訊。

06:35

Or 3. You could visit a store if the company is a B2C one.

或者 3. 如果公司是 B2C 企業,你可以親自造訪一家門市。

06:40

Takeaway number three, unconventional wisdom one.

第三個重點,非常規智慧之一。

06:44

Dividends don't matter.

股息並不重要。

06:47

Philip Fisher questions many of the truths that the general public has come to accept within the field of investing.

菲利普·費雪質疑了許多公眾在投資領域中普遍接受的真理。

06:54

One of these truths is the overconfidence in dividends.

其中一個真理就是對股息的過度自信。

06:58

According to Fisher, dividends are one of the least important aspects when it comes to making an investment decision.

根據費雪的觀點,在做出投資決策時,股息是最不重要的因素之一。

07:04

Let's break down this issue.

讓我們來分析這個問題。

07:06

The only reason why a company should pay you dividends, assuming that you aren't broke and in need of a quick buck to pay your groceries— by the way, then you shouldn't put that money in stocks in the first place— is if it increases the value for you as a stock owner.

There are plenty of other valuable things that the company could do for its investors with excess capital, instead of handing them out as dividends.

公司有很多其他有價值的事情可以為投資者做,而不是將多餘的資本作為股息發放。

07:29

For instance, it could invest in a global expansion, spend capital in R&D to find new lucrative products, increase production efficiency, reducing production costs, advertise more, getting more customers, hiring more competent employees.

If the management has found a potentially better use of its capital, you should be pleased as an investor, not nagging about missing out on dividends.

如果管理層發現了資本的潛在更佳用途,作為投資者,你應該感到高興,而不是抱怨錯過了股息。

07:58

Here's another example on why current dividends isn't interesting.

以下是另一個例子,說明為什麼當前的股息並不吸引人。

08:02

Company A has a stock value that $10, and paying a dividend of $0.5, which equals to a 5% yield per year.

A 公司的股票價值為 10 美元,並支付 0.5 美元的股息,相當於每年 5% 的收益率。

08:10

Company B is also a stock value that $10, but pays a dividend of $0.2, which equals to a 2% yield per year.

B 公司的股票價值也是 10 美元,但支付 0.2 美元的股息,相當於每年 2% 的收益率。

08:18

Initially, one might assume that Company A is a better investment than Company B, but let's look at what happens in the following 10 years with the two companies.

最初,人們可能會認為 A 公司比 B 公司更適合投資,但讓我們看看接下來的 10 年中這兩家公司的表現。

08:28

Company A grew like the market tends to do in general, by about 7% per year.

公司A的成長速度與市場整體趨勢相符,每年約成長7%。

08:34

Therefore, it's now valued at $20, and the dividend yield has been kept at 5%, so the current dividend is $1 per year.

因此,它現在的價值為20美元,股息率保持在5%,所以目前的股息是每年1美元。

08:42

Now let's consider Company B.

現在讓我們來看看公司B。

08:44

This was a growth stock, which ticked all of Fisher's 15 boxes, and therefore it's been able to grow much faster than the underlying market.

這是一支成長股,符合費雪的15項標準,因此它能夠比市場整體成長得更快。

08:53

Its annual growth has been 26%, and therefore the stock is now valued 10 times its initial price, which equals to $100 per share.

它的年成長率為26%,因此股價現在是初始價格的10倍,即每股100美元。

09:02

Company B has also kept its dividend policies.

公司B也保持了其股息政策。

09:06

It's still yielding 2% per year, but that means that the dividend is now $2 per year.

它仍然每年提供2%的股息率,但這意味著現在的股息是每年2美元。

09:12

I hope you see what I'm getting at here.

希望你能理解我的意思。

09:14

Company A now has a dividend of 10% on your initial investment, while Company B has a dividend of 20% of your original purchase.

公司A現在的股息相當於你初始投資的10%,而公司B的股息則是你原始購買價的20%。

09:23

So don't stare yourself blind on dividends.

所以不要只盯著股息看。

09:26

Current dividends don't stand a chance against future growth prospects.

當前的股息無法與未來的成長前景相提並論。

09:32

Takeaway number four, unconventional wisdom too.

第四個要點,也是非傳統的智慧。

09:36

You are diversifying too much.

你的投資組合過於多元化。

09:38

Here's another truth that many investors have come to accept.

這是許多投資者已經接受的另一個事實。

09:43

Diversifying, diversifying, diversifying.

多元化,多元化,多元化。

09:47

The one universal rule that idiots in finance know is diversification.

金融領域的白痴都知道的唯一普遍規則就是多元化。

09:51

If you owe me free lunch, you've got to diversify.

如果你欠我一頓免費午餐,你就得多元化。

09:54

Diversification is crucial, and the more diversification you can get, the better.

多元化至關重要,而且你能獲得的多元化越多越好。

09:59

Single stocks are a bad place to invest money.

單一股票不是投資資金的好地方。

10:01

They're much better off to be spread out and well diversified.

它們更適合被分散並且多元化。

10:05

Philip Fisher argues that people overstress you shouldn't put all your eggs into one basket.

菲利普·費雪認為,人們過度強調不要把所有雞蛋放在一個籃子裡。

10:10

The horrors of what could happen if you don't follow the advice is exaggerated for an active investor, and the other end of the extreme is not mentioned often enough.

對於積極投資者來說,如果不遵循這個建議可能會發生的可怕後果被夸大了,而另一個極端卻沒有被經常提及。

10:19

If you're having eggs in too many baskets, many of them end up in quite mediocre or unattractive ones, and you'll never be able to watch them carefully.

Investors who are oversold on diversification put far too little money into companies they thoroughly understand, and far too much in others, about which they know nothing at all.

Because of this restriction, which I've yet to find a loophole for, but you know, I'm searching, the more companies you have, the less you know about each of them.

Furthermore, when people give you the advice to say, invest in 15 companies to be diversified, they have misunderstood what diversification is about, which is spreading your risks.

此外,當人們給你建議說,投資15家公司才能多元化時,他們誤解了多元化的含義,即分散你的風險。

11:04

There are many other factors to consider, such as do the companies in your portfolio operate in different industries?

有許多其他因素需要考慮,例如你的投資組合中的公司是否在不同的行業運營?

11:11

For instance, a portfolio like this one is not spreading your risks, even though it contains 15 companies.

例如,像這樣的投資組合並沒有分散你的風險,儘管它包含了15家公司。

11:18

Do the companies in your portfolio have multiple branches or brands?

你的投資組合中的公司是否有多個分支或品牌?

11:22

For instance, comparing Dow DuPont to something like Snapchat or Spotify would be just short of silly.

例如,將道瓊杜邦與Snapchat或Spotify進行比較簡直是愚蠢的。

11:29

Dow DuPont is well diversified in itself.

道瓊杜邦本身就具有良好的多元化。

11:33

Are the companies of sufficient size?

這些公司的規模是否足夠大?

11:35

Smaller companies tend to be one man shows more often than larger ones, and therefore requires more diversification, as you can never know what will happen to a single person.

To evaluate any investment opportunity takes a considerable amount of work.

評估任何投資機會都需要大量的工作。

11:59

Evaluating all of Fisher's 15 points for every publicly traded company in the world would be complete madness.

對世界上每家上市公司評估費雪的所有15點將是完全瘋狂的。

12:06

You'd spend too much time researching cases that you could have dropped much earlier.

你會花太多時間研究那些你本可以更早放棄的案例。

12:11

Therefore, you need a process that can quickly separate the winners from the losers.

因此,你需要一個能夠快速區分贏家和輸家的過程。

12:15

You need to know that you're fishing in the right pond.

你需要知道自己是在正確的池塘裡釣魚。

12:18

In investing, this process is called screening.

在投資中,這個過程稱為篩選。

12:22

To make big money on investments, it's unnecessary to get some answer to every investment that might be considered.

要在投資中賺大錢,不需要對每一個可能考慮的投資都得到答案。

12:29

What is necessary is to get the right answer a large proportion of the very small number of times actual purchase are made.

必要的是,在實際購買的極少數情況下,能得到正確的答案。

12:38

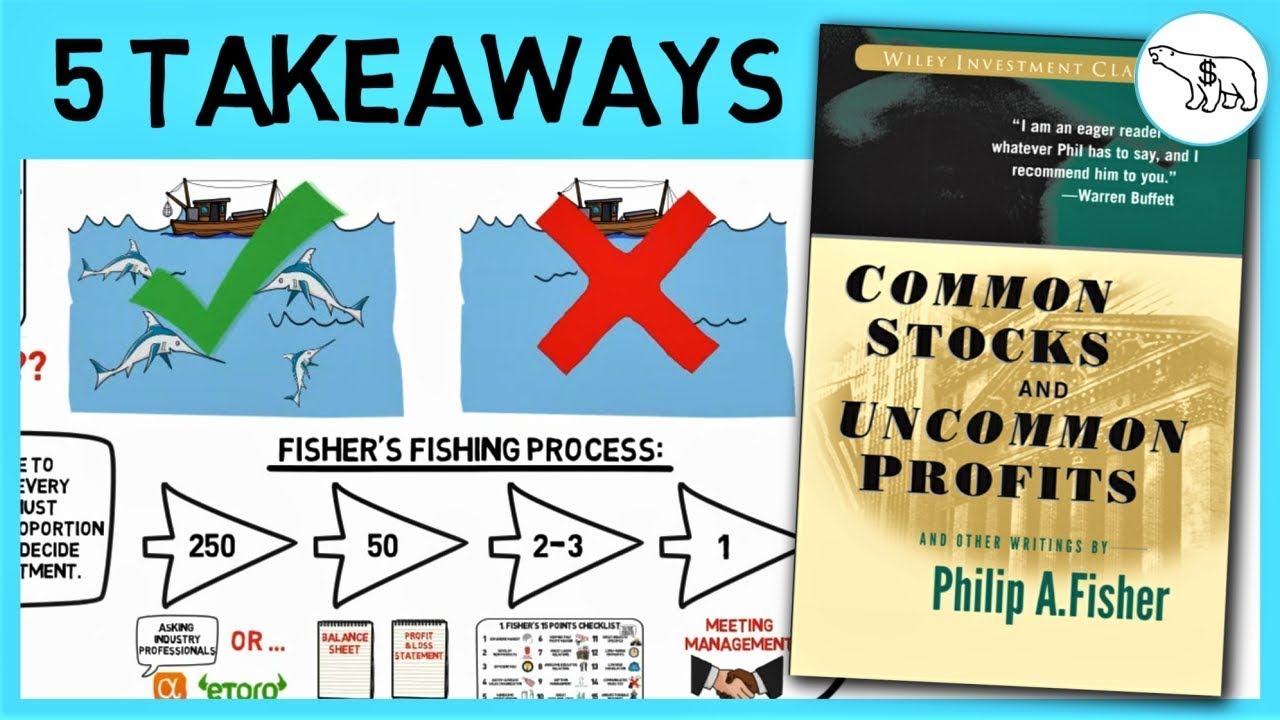

Here's how Fisher approaches the stock-picking process.

以下是費雪如何進行選股過程。

12:41

Firstly, he talks to people within the investing industry.

首先,他會與投資業內的人士交談。

12:45

He will consider around 250 companies from various sources of people that he trusts in the industry.

他會從業內他信任的人士那裡考慮約250家公司。

12:51

For the average investor, they might not have such connections yet, but today there's another solution.

對於普通投資者來說,他們可能還沒有這樣的關係,但今天有另一個解決方案。

12:57

There are many social investment platforms out there, such as Seeking Alpha or Etoro.

現在有許多社交投資平台,例如Seeking Alpha或Etoro。

13:02

Follow the people you find trustworthy on these platforms and let them help you during the initial part of the screening process.

在這些平台上關注你認為可信的人,讓他們在篩選過程的初期階段幫助你。

13:09

After this, Fisher aims to transform the list of 250 companies to approximately 50.

之後,費雪的目標是將250家公司的名單縮減到約50家。

13:16

At this stage, he won't do a deep dive yet, but he will glance over the balance sheet, look at the breakdown of total sales by product lines, profit margins, and the competition.

在此階段,他還不會進行深入研究,但會瀏覽資產負債表,查看產品線的總銷售額分解、利潤率和競爭情況。

13:27

Now, we're finally ready for the Scuttlebutt.

現在,我們終於準備好進行「Scuttlebutt」了。

13:30

Out of 50 companies, only two to three of them will survive.

在50家公司中,只有兩到三家能夠通過。

13:34

Yes, that is how hard it is to take all of Fisher's 15 boxes.

是的,這就是通過費雪所有15個檢查點的難度。

13:38

As mentioned previously, suppliers, customers, research scientists, trade associations, and former employees are great sources of information here.

如前所述,供應商、客戶、研究科學家、行業協會和前員工都是此處的重要信息來源。

13:48

And then, there is the final stage.

然後,進入最後階段。

13:51

This is visiting the management of the business.

這就是拜訪公司管理層。

13:54

Out of two to three companies visited, Fisher typically invested in only one of them.

在拜訪的兩到三家公司中,費雪通常只會投資其中一家。

13:59

This is truly a thorough process to go through in order to find one single company, and I think it shows quite clear why Fisher is considered one of the greatest of all time.

We will definitely talk more about screening and fishing in the right pond in the future.

我們以後一定會更深入地討論如何篩選和在正確的池塘中釣魚。

14:16

So, what do you think about the takeaways?

那麼,你覺得這些要點如何?

14:18

Are all of the 15 points as valuable today, as they were 50 years ago, when this book was first released?

這15點在今天是否和50年前這本書首次出版時一樣有價值?

14:25

I should also mention that there are many more takeaways that I didn't have room for in this summary.

我還應該提到,這個摘要中還有許多其他要點我沒有空間列出。

14:29

If you would like to have the full read, I would appreciate if you use the affiliate link below.

如果你想完整閱讀這本書,希望你能使用下方的聯盟連結。

14:34

In that way, you'll sponsor this channel and benefit your future self at the same time.

這樣,你既能支持這個頻道,又能造福未來的自己。

14:40

If you enjoyed this video, don't forget to check out my latest one.

如果你喜歡這個影片,別忘了看看我的最新影片。

14:43

Also, if you're interested in more animated summaries on investment classics, I've got a video of The Intelligent Investor by Benjamin Graham that you definitely must check out.